Tax season is upon us, and you might be wondering if filing a tax extension is the right move for you this year.

At 7B Bookkeeping & Tax LLC, we often get questions about tax extensions and their implications.

This blog post will break down the pros and cons of filing for an extension, helping you make an informed decision about your taxes.

Understanding Tax Extensions

What Is a Tax Extension?

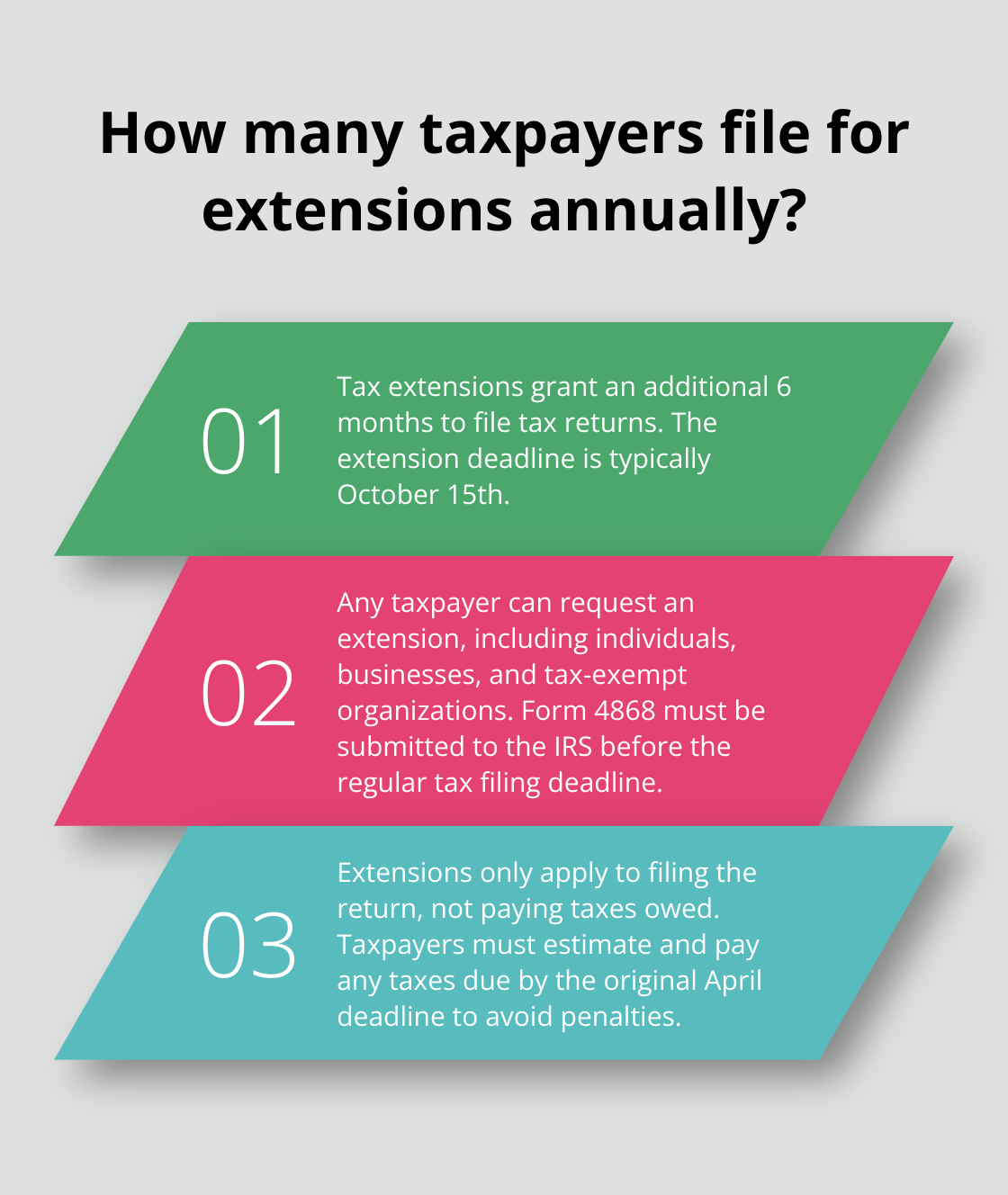

A tax extension allows taxpayers to request additional time from the Internal Revenue Service (IRS) to file their tax return. This extension applies only to the filing of the return, not to the payment of taxes owed. The IRS automatically grants extensions to taxpayers who request them, providing an additional 6 months to complete and submit tax forms.

Who Can File for an Extension?

Any taxpayer can file for an extension, regardless of income level or filing status. This includes:

- Individuals

- Businesses

- Tax-exempt organizations

The IRS does not require a reason for requesting an extension, making it accessible to everyone who needs more time.

How to Request an Extension

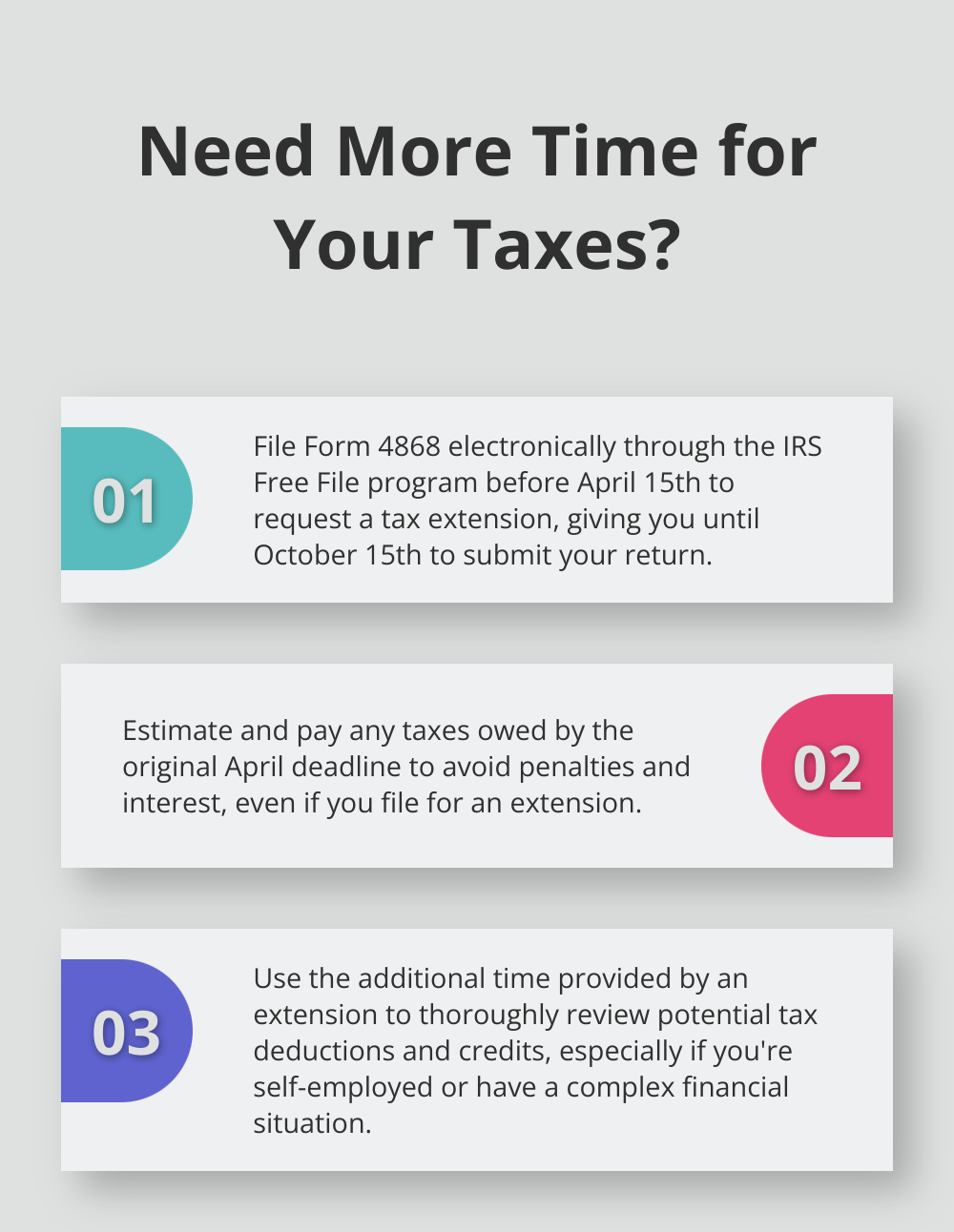

To request an extension, taxpayers must submit Form 4868 to the IRS before the regular tax filing deadline (typically April 15th). Options for filing this form include:

- Electronic submission through the IRS Free File program

- Mailing a physical form

- Using tax preparation software with built-in extension filing options

The Six-Month Grace Period

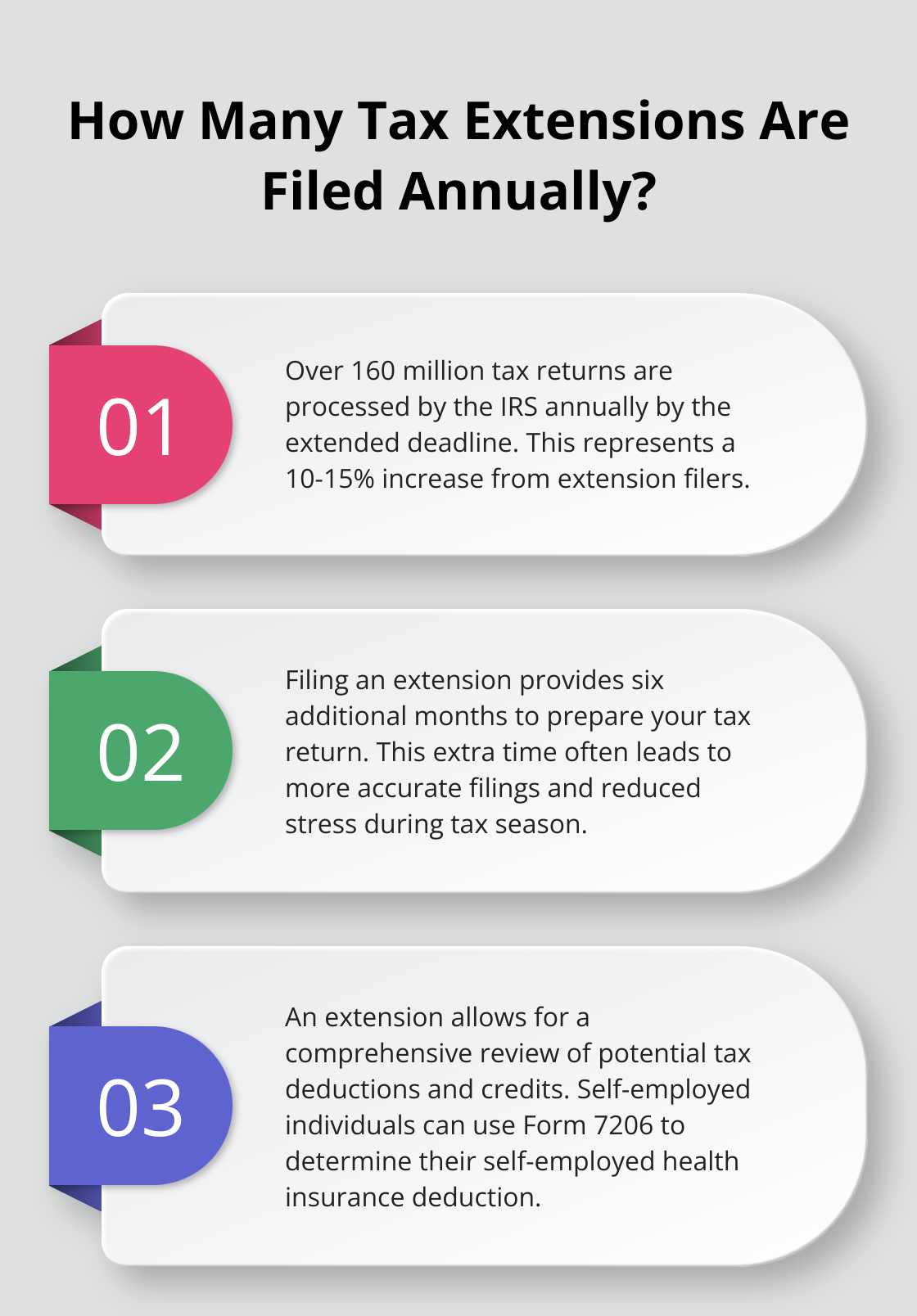

An approved tax extension provides taxpayers until October 15th to file their return. This additional time proves valuable for those missing important documents or needing extra time to prepare an accurate return. However, it’s essential to note that taxpayers must still estimate and pay any taxes owed by the original April deadline to avoid penalties and interest.

IRS data shows that many taxpayers file for extensions each year, highlighting the widespread use and utility of this option for many Americans.

As we move forward, let’s examine the advantages of filing a tax extension and how it can benefit taxpayers in various situations.

Benefits of Filing a Tax Extension

Filing a tax extension can provide significant advantages for many taxpayers. Let’s explore the key benefits of requesting more time to file your taxes.

Reduced Stress and Improved Accuracy

One of the primary benefits of filing an extension is the reduction of stress during tax season. With six additional months to prepare your return, you can take the time to gather all necessary documents and review your financial records thoroughly. This extra time often leads to more accurate filings, potentially saving you from costly errors or omissions.

IRS data shows that by the extended deadline, the IRS processes over 160 million returns annually, a 10–15% increase from extension filers. This increased accuracy can help you avoid triggering an audit or having to file an amended return later.

Maximized Tax Deductions and Credits

The additional time provided by an extension allows for a more comprehensive review of potential tax deductions and credits. Many taxpayers miss out on valuable opportunities to reduce their tax liability simply because they’re pressed for time.

For example, self-employed individuals can use this extra time to thoroughly categorize expenses and identify all possible deductions. The IRS provides Form 7206 and its instructions to determine any amount of the self-employed health insurance deduction you may be able to claim and report on Schedule 1.

Flexibility for Complex Financial Situations

If you’ve experienced significant life changes or have a complex financial situation, an extension can be particularly beneficial. This might include:

- Starting a new business

- Selling property or investments

- Experiencing major life events (like marriage, divorce, or the birth of a child)

These situations often require additional documentation or professional consultation to ensure proper reporting. The extra time allows you to navigate these complexities without the pressure of an imminent deadline.

Strategic Tax Planning Opportunities

An extension provides more time for strategic tax planning. This can be especially valuable for high-income earners or those with complex investment portfolios. The additional months allow for a thorough analysis of various tax strategies and their potential impact on your overall financial picture.

For instance, you might use this time to:

- Evaluate the tax implications of different investment decisions

- Consider the timing of certain financial transactions

- Explore opportunities for tax-loss harvesting

While an extension offers numerous benefits, it’s important to understand its limitations. The next section will explore potential drawbacks to consider when deciding whether to file for an extension.

The Hidden Costs of Tax Extensions

Payment Deadline Remains Unchanged

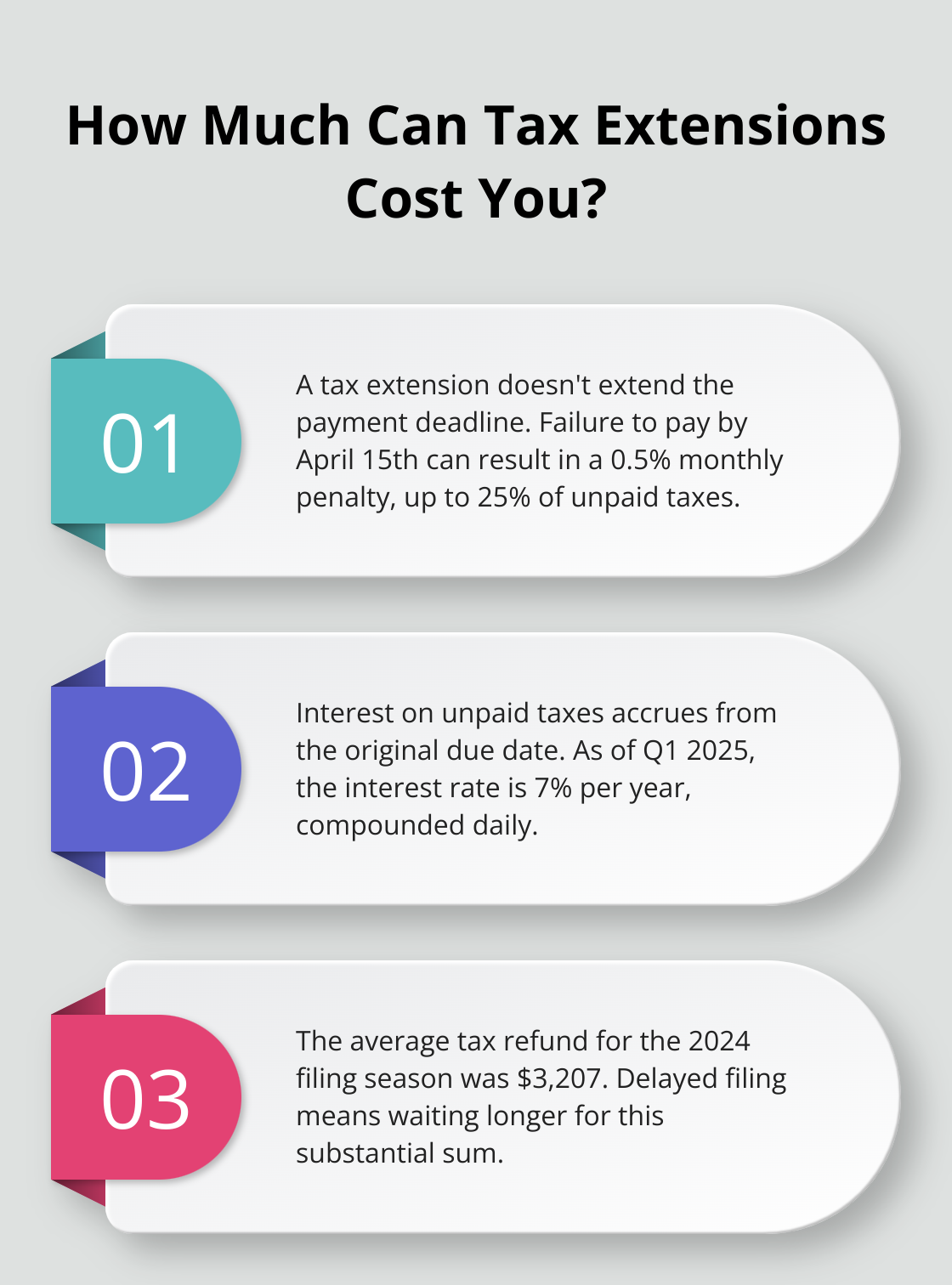

A tax extension does not provide extra time to pay taxes owed. The Internal Revenue Service (IRS) expects you to pay any estimated taxes by the original deadline (typically April 15th). Failure to pay on time can result in penalties and interest charges that accumulate over time.

For instance, if you owe $5,000 in taxes and don’t pay by the original deadline, you could face a failure-to-pay penalty of 0.5% of the unpaid taxes for each month (or part of a month) the tax remains unpaid. This penalty can reach up to 25% of your unpaid taxes.

Interest Charges Accumulate Quickly

Even with an extension, interest on unpaid taxes starts to accrue from the original due date. The IRS determines the interest rate quarterly, and it can fluctuate. As of the first quarter of 2025, the interest rate for underpayments stands at 7% per year, compounded daily. This means your tax debt can grow significantly if left unpaid for an extended period.

Delayed Refunds Impact Financial Planning

If you expect a tax refund, filing an extension means you’ll wait longer to receive your money. This delay can affect your financial planning, especially if you counted on that refund for important expenses or investments.

IRS data shows that the average tax refund for the 2024 filing season was $3,207 (as of February 16, 2024). That’s a substantial amount that could be put to good use sooner rather than later.

Increased Risk of Errors

While an extension provides more time to file, it also increases the risk of misplacing important tax documents or forgetting about certain income sources. This can lead to errors on your tax return, which may trigger audits or result in additional penalties.

Missed Opportunities for Early Planning

Filing an extension can delay important financial decisions. Early tax filing allows you to identify areas for improvement in your financial strategy for the current year. By postponing your filing, you might miss opportunities to adjust your withholdings, change your investment strategy, or make other financial decisions that could benefit you in the long run.

Final Thoughts

A tax extension provides extra time to gather documents and maximize deductions, but it doesn’t extend the payment deadline. You could face penalties and interest if you don’t pay estimated taxes by the original due date. Your specific financial situation should guide your decision to file an extension.

We at 7B Bookkeeping & Tax LLC offer expert guidance on tax extensions and comprehensive financial services. Our team can help you navigate the intricacies of tax filing, ensuring you make the best decision for your financial future. We encourage you to consult with a tax professional before deciding on an extension.

Stay proactive about your taxes throughout the year. Keep accurate records, stay informed about tax law changes, and seek professional help when needed. These steps will prepare you to handle your tax obligations, regardless of when you file (with or without an extension).