Account reconciliation is a cornerstone of sound financial management. At 7B Bookkeeping & Tax LLC, we’ve seen firsthand how this practice can transform a business’s financial health.

In this guide, we’ll explore why regular account reconciliation is essential and provide a step-by-step approach to mastering this critical process. Whether you’re a small business owner or a financial professional, understanding and implementing effective reconciliation techniques can significantly impact your financial accuracy and decision-making.

What Is Account Reconciliation?

Account reconciliation compares internal financial records with external statements to ensure accuracy and identify discrepancies. This financial practice helps businesses maintain precise records and detect potential errors or fraudulent activities.

Types of Accounts Requiring Reconciliation

Several account types demand regular reconciliation:

- Bank accounts: These involve numerous transactions and are prone to discrepancies.

- Credit card accounts: Regular checks catch unauthorized charges or billing errors.

- Accounts payable and receivable: Reconciliation ensures accurate recording of all invoices and payments.

- Stock accounts: For businesses with inventory, reconciliation prevents shrinkage and maintains accurate valuation.

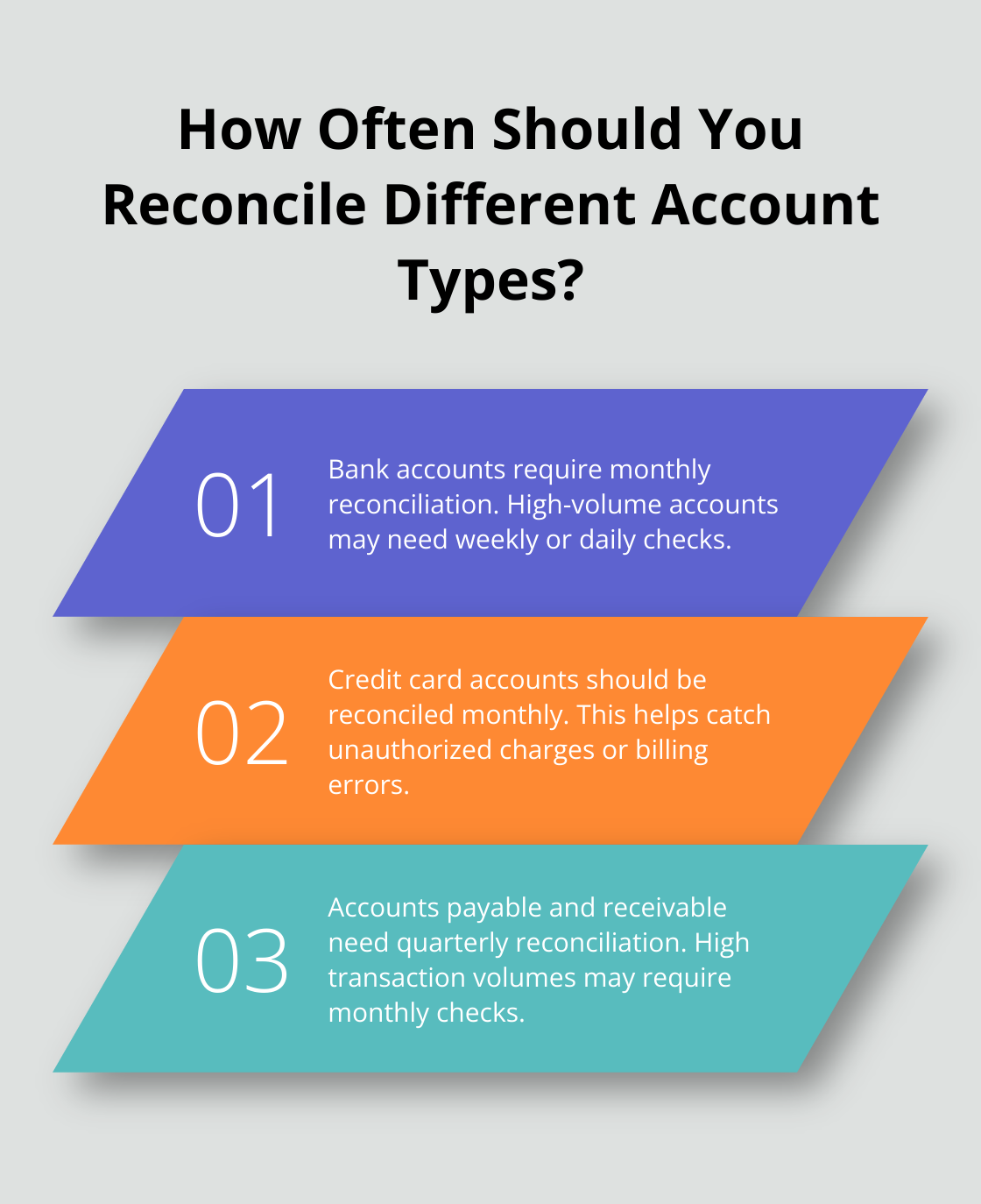

Frequency of Reconciliation

The reconciliation frequency varies depending on the account type and transaction volume:

- Bank accounts: Monthly reconciliation (aligning with statement cycles)

- High-volume accounts: Weekly or daily checks

- Credit card accounts: Monthly reconciliation

- Accounts payable and receivable: Quarterly (or monthly for high transaction volumes)

- Inventory accounts: During physical counts (monthly to annually, depending on business type and size)

Tools for Efficient Reconciliation

Modern accounting software (like QuickBooks Online) streamlines the reconciliation process. These tools often feature automated matching algorithms that quickly identify discrepancies, saving time and reducing human error. However, human oversight remains essential for interpreting results and addressing complex issues.

Benefits of Regular Reconciliation

Regular account reconciliation offers numerous advantages:

- Early error detection: Catch and correct mistakes before they compound.

- Fraud prevention: Identify suspicious activities promptly.

- Improved financial accuracy: Ensure your financial statements reflect reality.

- Better cash flow management: Maintain an accurate picture of your financial position.

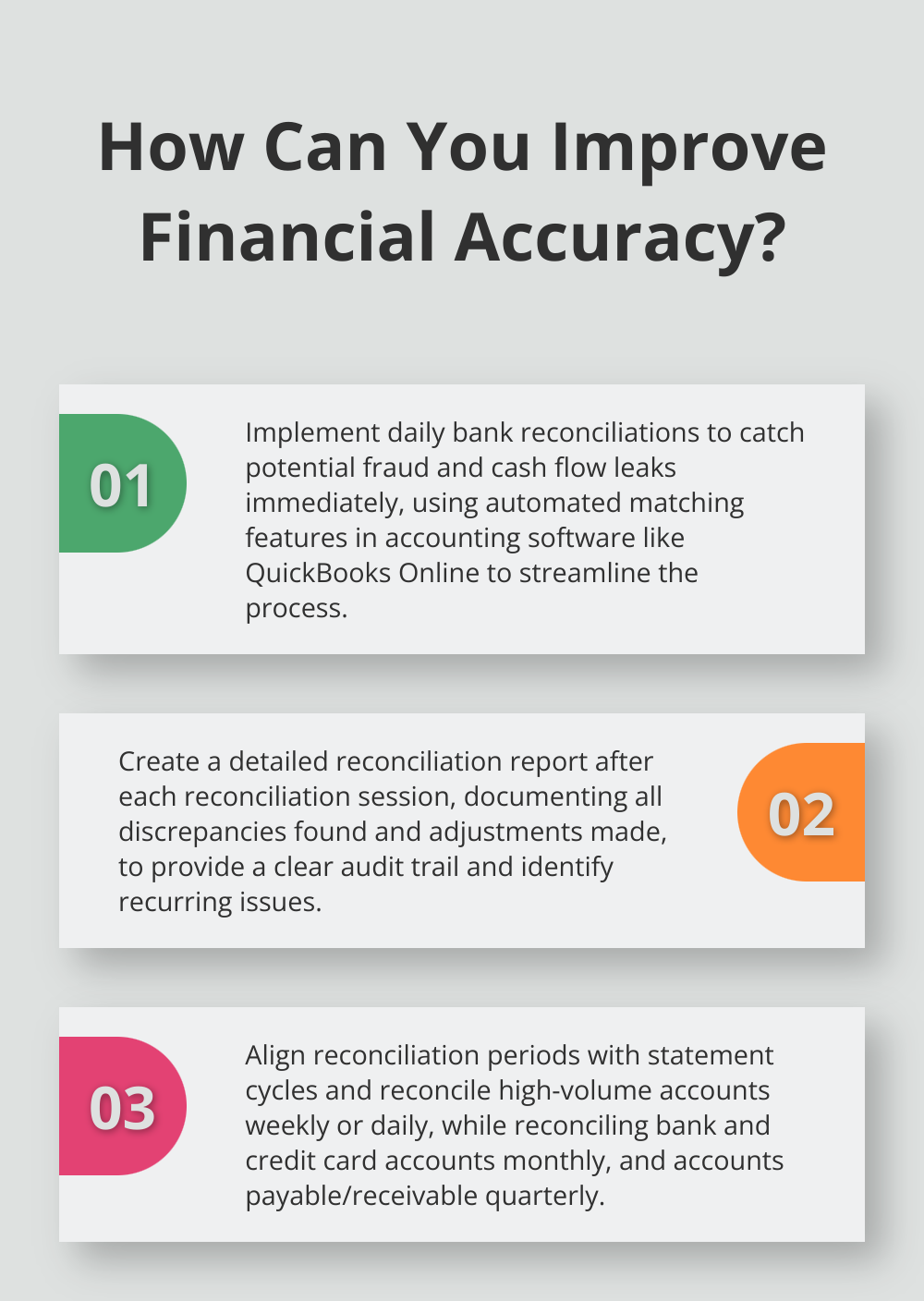

Regular reconciliation forms the foundation of sound financial management. By working through bank reconciliations daily, it’s possible to catch potential fraud and cash flow leaks immediately. The next section will explore the specific benefits of this practice in more detail, highlighting why it’s a non-negotiable aspect of business finance.

Why Regular Account Reconciliation Matters

Regular account reconciliation transforms businesses of all sizes. This practice extends beyond basic bookkeeping-it serves as a powerful tool for financial health and strategic decision-making.

Early Error Detection

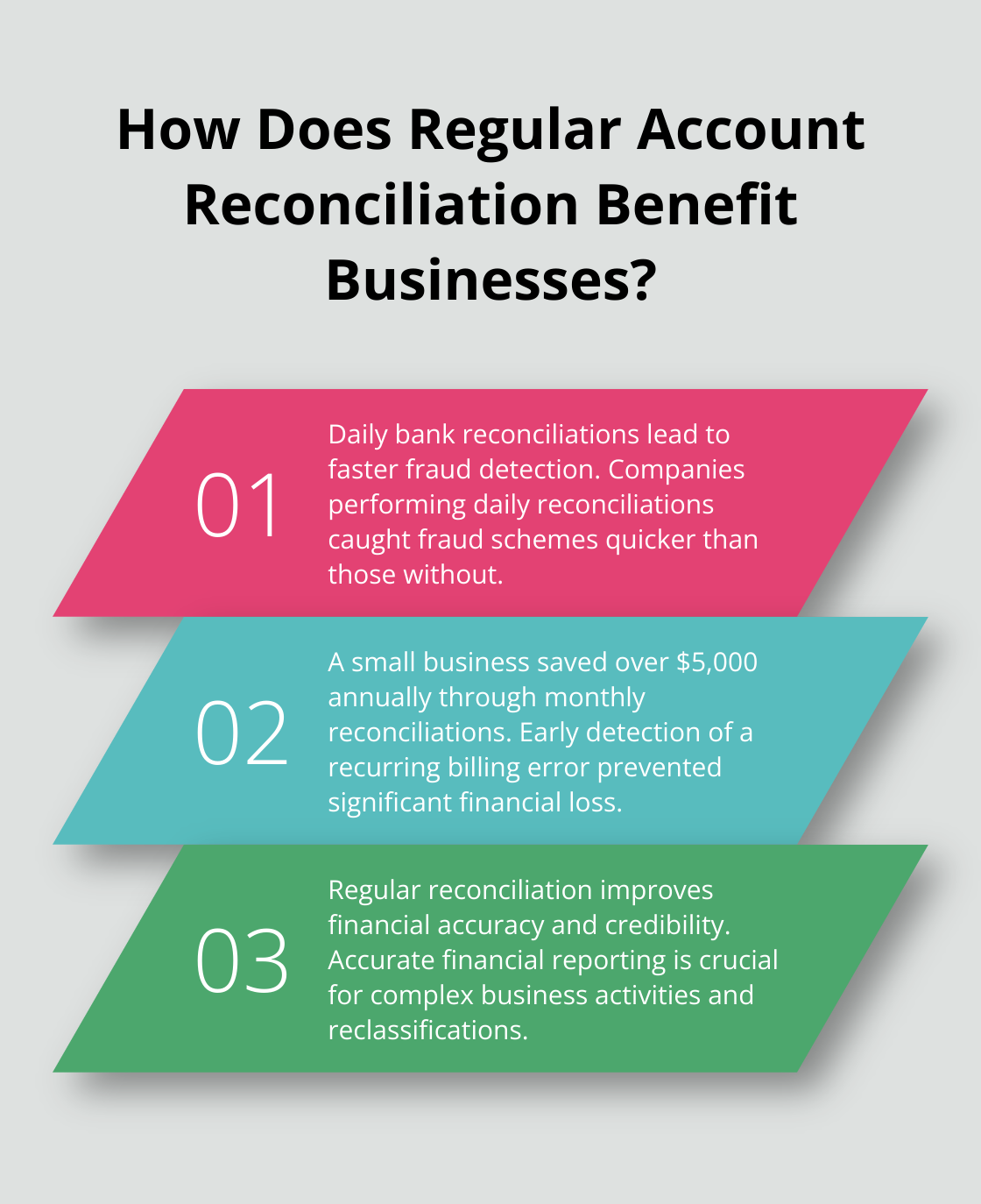

Frequent reconciliation allows for swift error detection. A 2022 survey by the Association of Certified Fraud Examiners found that companies performing daily bank reconciliations detected fraud schemes faster than those without. This rapid detection can save businesses thousands of dollars in potential losses.

A small business owner discovered a recurring billing error through monthly reconciliations. This early catch saved them over $5,000 annually-money they would have lost if reconciliation occurred less frequently.

Enhanced Financial Accuracy

Accurate financial reporting enables informed business decisions. Regular reconciliation ensures that financial statements reflect the true state of a business. A recent report highlighted the importance of accurate financial reporting, especially when dealing with complex business activities and reclassifications.

This improved accuracy builds credibility with external stakeholders (such as investors, lenders, and regulatory bodies). Consistently accurate financial reports position businesses better to secure funding, pass audits, and maintain compliance.

Optimized Cash Flow Management

Effective cash flow management fuels any business. Regular account reconciliation provides a clear, up-to-date picture of a company’s financial position. This real-time insight allows for more agile financial planning and helps prevent cash flow crises.

A retail sector client implemented weekly reconciliations during their peak season. This practice allowed them to identify and address slow-paying customers more quickly, reducing their average collection period by 15 days. The result? A significant improvement in their working capital and ability to manage seasonal inventory purchases.

Strengthened Fraud Prevention

While no business wants to consider fraud, it remains a reality that requires attention. Regular reconciliation acts as a powerful deterrent and detection tool.

Frequent account reconciliation creates multiple checkpoints where fraudulent activities can surface. This practice not only helps catch external fraud attempts but also deters internal misconduct. Employees are less likely to attempt fraud when they know accounts undergo regular scrutiny.

A robust reconciliation process safeguards a business’s financial integrity and future. The next section will provide a step-by-step guide to implementing effective account reconciliation practices, ensuring you can harness these benefits for your own business.

How to Perform Account Reconciliation

Account reconciliation is a critical process that ensures the integrity of your financial data. By following these steps and maintaining consistency, you can build a strong foundation for financial accuracy and informed decision-making.

Prepare Your Documents

Start by collecting all necessary financial documents. These typically include bank statements, credit card statements, and your company’s general ledger. For digital records, export reports from your accounting software. QuickBooks Online offers easy-to-generate reports for this purpose.

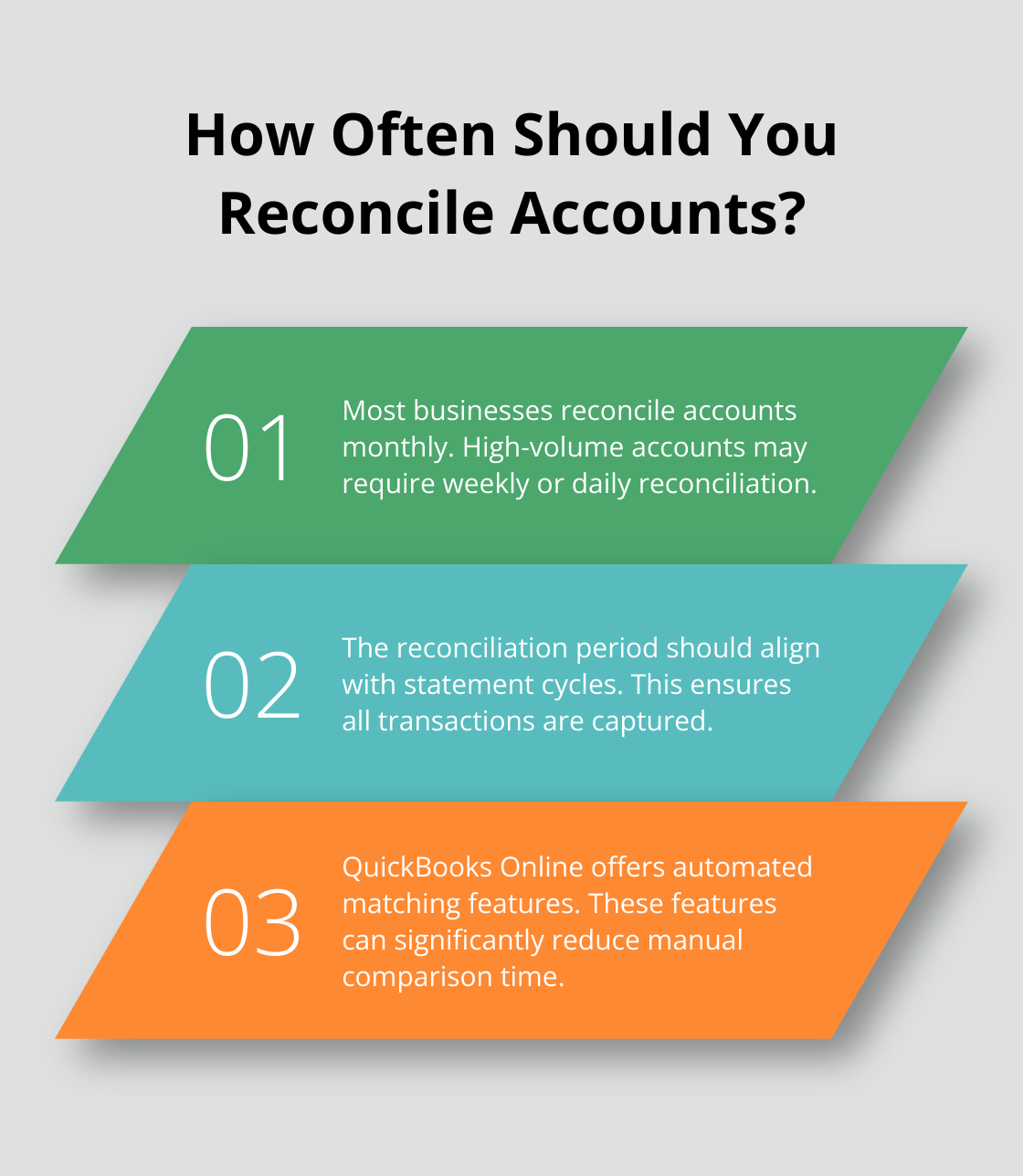

Next, determine the reconciliation period. Most businesses reconcile accounts monthly, but high-volume accounts may require weekly or daily reconciliation. Choose a cutoff date that aligns with your statement cycles to ensure all transactions are captured.

Compare and Contrast

With your documents ready, begin to compare your internal records with external statements. Look at each transaction, match amounts and dates. Pay close attention to deposits, withdrawals, and any fees or interest charges.

Modern accounting software can streamline this process. For instance, QuickBooks Online offers automated matching features that can significantly reduce the time spent on manual comparisons. However, don’t rely solely on automation. Human oversight remains important for catching nuanced discrepancies.

Investigate Discrepancies

As you compare records, you’ll likely encounter discrepancies. These can range from simple timing differences to more complex issues like unrecorded transactions or errors. Don’t panic – discrepancies are common and often easy to resolve.

For each discrepancy, investigate the root cause. Did a check not clear? Did a deposit clear after the statement date? Are there any duplicate entries? Document each discrepancy and its cause for future reference.

Make Necessary Adjustments

Once you’ve identified and investigated discrepancies, it’s time to make adjustments. This might involve entering missing transactions, correcting errors, or making journal entries to account for timing differences.

Be meticulous in your adjustments. Each change should have clear documentation and justification. If you’re unsure about how to handle a particular adjustment, consult with a professional. (Many businesses find value in expert guidance for complex reconciliation issues.)

Document the Process

The final step is thorough documentation. Create a reconciliation report that outlines the process, lists all discrepancies found, and details the adjustments made. This documentation serves multiple purposes:

- It provides a clear audit trail for internal and external reviews.

- It helps identify recurring issues that may need systemic solutions.

- It serves as a reference for future reconciliations.

Store these reports securely, either in a physical file or a secure digital system. (QuickBooks Online allows you to attach notes and documents to reconciliation reports, creating a comprehensive record.)

Account reconciliation is not just about matching numbers. It’s a critical process that ensures the integrity of your financial data. Try to follow these steps and maintain consistency to build a strong foundation for financial accuracy and informed decision-making.

Final Thoughts

Account reconciliation forms the foundation of robust financial management. This practice allows businesses to detect errors early, improve financial accuracy, optimize cash flow, and prevent fraud. Regular reconciliation supports informed decision-making and builds credibility with stakeholders, ensuring the integrity of financial data.

Implementing effective reconciliation processes can challenge small businesses or those with complex financial structures. Professional assistance can make a significant difference in these situations. 7B Bookkeeping & Tax LLC offers comprehensive financial services, including expert account reconciliation, to streamline your processes and ensure accuracy and compliance.

Our flat-rate bookkeeping service includes regular account reconciliation using QuickBooks Online. We also provide QuickBooks setup and training to empower you to manage your finances more effectively. Don’t let the complexities of account reconciliation hinder your business growth; consider seeking professional support to ensure its effective implementation.